Same Principles, New URL

Michael Preysman found out that Everlane had been sold to Shein the same way most people did, through the noise of a news cycle rather than a boardroom conversation. He was executive chair until earlier this year. He co founded the company in 2011. He ran it for eleven years. And yet when the transaction that ended Everlane’s independent existence was agreed, the shareholder note reportedly went out on a Sunday morning and Preysman, by his spokesperson’s own account, was “appalled.”

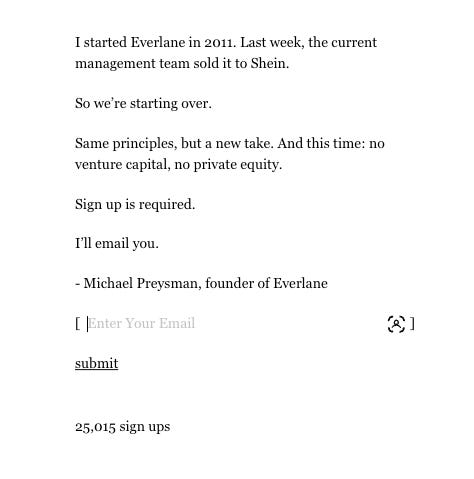

The easy reading of Still Radical is that this is a founder coming back to reclaim the moral story of the company he started. The brand is currently little more than a landing page collecting emails, with a name that clearly nods to Everlane’s old promise of radical transparency. The principled visionary, exiled from his creation, watches in horror as it is sold to the antithesis of everything he built, and rises to try again. It is a clean story. It is also almost certainly a constructed one, and the construction is doing a great deal of work that deserves examination before twenty five thousand email addresses become thousands of paying customers.

The question is not whether Preysman is sincere. The question is what sincerity means when the person expressing it spent three years as executive chair of a company that, by all available accounts, was already on its trajectory toward Shein before he formally departed. The venture capital and private equity that Preysman now disavows were structural features of Everlane’s capital architecture while he was sitting on its board. The quality declines and supply chain compromises that disappointed Everlane’s customers did not begin the morning Alfred Chang was hired. They began during a period of capital pressure and leadership transition that Preysman was, at minimum, proximate to. The Shein acquisition was the conclusion of a process, not the initiation of one.

This is not a moral indictment. It is a structural observation, and the distinction matters precisely because Still Radical’s opening premise requires it to be taken as the former. The implicit argument is that the principles were right, the capital structure was the corruption, and now that the capital structure has been changed, the principles can be properly expressed. That logic only holds if the principles were, in fact, intact during the period in which the capital structure was corroding them. The evidence for this is, to put it charitably, thinner than a landing page collecting emails.

What is genuinely interesting about Still Radical is not the founding narrative but the specific constraint Preysman has announced: no venture capital and no private equity. On its face, this sounds like a governance commitment. In practice, it is an admission that the previous governance structure was incompatible with the mission, paired with a conspicuous absence of any explanation of what replaces it. Saying “no venture capital and no private equity” is the equivalent of a restaurant announcing that it will no longer use a microwave. Correct diagnosis, but the cuisine still has to come from somewhere, and the sourcing, preparation, and economics of the alternative have not yet been disclosed.

The financing alternatives available to a consumer brand in 2026 that refuses venture capital and private equity are not especially numerous. Revenue based financing links repayment to top line performance, which creates its own growth pressure, albeit less acute. Cooperative or steward owned structures are structurally superior for mission preservation but typically limit the pace of scaling and the pool of available capital. Bootstrapped growth is possible, but it implies either a product market fit so strong that the brand funds itself from day one, or a willingness to operate at a scale most of Everlane’s former customer base would find anticlimactic. Crowdfunding is available. Community investment is available. None of these is as clean as a landing page with a principled statement.

The radical move that Still Radical has not yet made, and the one that would genuinely distinguish it from its predecessor, is legal commitment. Benefit corporation status, cooperative bylaws, or a golden share structure that makes the mission legally binding rather than aspirationally maintained: these are the instruments that turn a founder’s stated values into a company’s structural DNA. Without them, “no venture capital and no private equity” is a preference, not a protection. A future CEO, hired by a future board that Preysman does not control, is under no legal obligation to honour it. The history of founder led brands in ethical fashion is substantially a history of exactly this kind of preference evaporating under commercial pressure. Preysman knows this. He watched it happen in slow motion for over a decade. The absence of any mention of structural safeguards in the Still Radical launch communication is, to put it plainly, the loudest thing about it.

There is also a timing problem that the warm reception to the email sign ups tends to obscure. Still Radical is arriving into a market that just watched Everlane, Allbirds, and a cohort of their ethical direct to consumer peers either collapse or capitulate within the same three year window. The consumer appetite for the idea of an ethical brand clearly persists. Twenty five thousand email addresses before a single product exists is real signal. But appetite for an idea and willingness to pay a premium for a product are different phenomena, and every brand in this space has discovered the gap between them in the most expensive possible way. The consumer who signed up for Everlane in 2015 was invited to believe they were participating in something that would grow, improve, and eventually change the way the industry operated. That belief now carries baggage. The product of that baggage is not the same kind of enthusiasm customers had the first time around. It is enthusiasm with a residue of prior disappointment, which is a harder thing to convert.

All of which makes Still Radical simultaneously the most natural thing Preysman could have done and the most interesting test the market for principled fashion has been given in years. If he builds it with genuine structural protection, real supply chain transparency rather than cost breakdown theatre, and a financing architecture that is legally constrained rather than voluntarily restrained, then the failure of Everlane might actually have produced something instructive. If he builds another beautifully photographed basics brand with a story about factories and margins, funded by some alternative instrument that produces the same growth pressure under a different name, then the lesson of Everlane will have been that the founder thought the problem was the instrument, when the problem was the incentive structure the instrument created. In that case, the incentive structure will have been repackaged, not removed.

Twenty five thousand email addresses and counting. The queue to be disappointed, or proved wrong, has already begun to form.

P.S. The most underreported element of this story is that Preysman was reportedly not involved in the decision to sell to Shein, despite having served as executive chair until earlier this year. Whatever the internal governance explanation for that, it is a fact that a company whose founding ethos was radical transparency completed the most consequential transaction in its history without, apparently, the knowledge of its founder.